The Impact of Student Loan Debt on Your Personal Finances

Student Loan Debt – Pay Now & Really Pay Later

Student loan debt is the #1 issue impacting the personal finances of most people under 30. According to a recent survey conducted by Student Loan Hero, the average student loan debt for 2016 graduates is now $37,172.

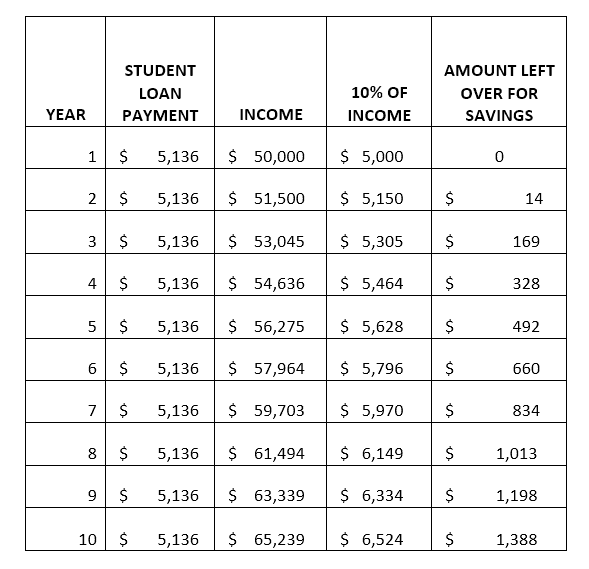

If you graduate with this amount of debt and we assume a 10 year repayment term at 6.8% interest, you’re looking at a monthly payment of $428 per month or $5,136 for a year. This is money that you need to shell out now at the expense of saving for retirement and other major purchases you’d like to make in the future.

The Impact on Retirement Savings

Those of you who regularly read my posts know that I love seeing “how the math works out.” For this situation, let’s assume that you:

- Need to make the $5,136 in student loan payments for 10 years

- Make an initial starting salary of $50,000

- Get a 3% raise every year

- Plan on using 10% of your income to either pay down debt or save for retirement

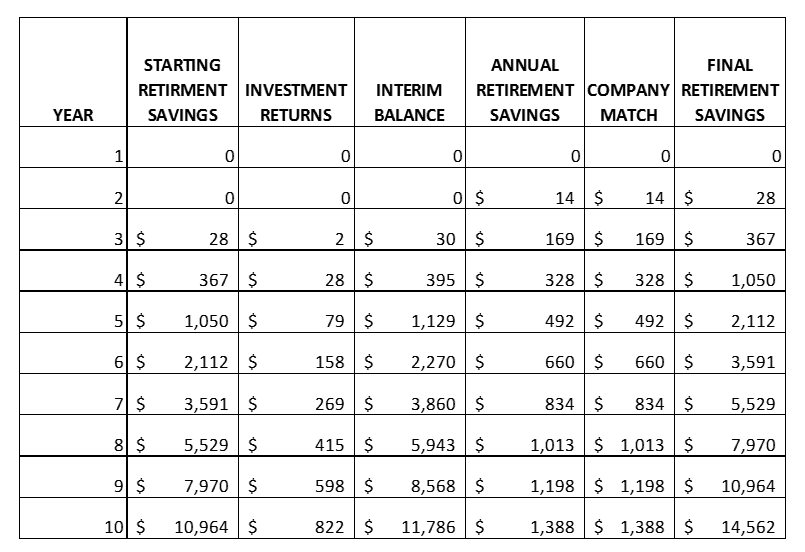

- Get a job with a company that offers a 401(k) with a 3% matching contribution.

Can earn a 7.50% return every year on your investments within your 401(k) plan.

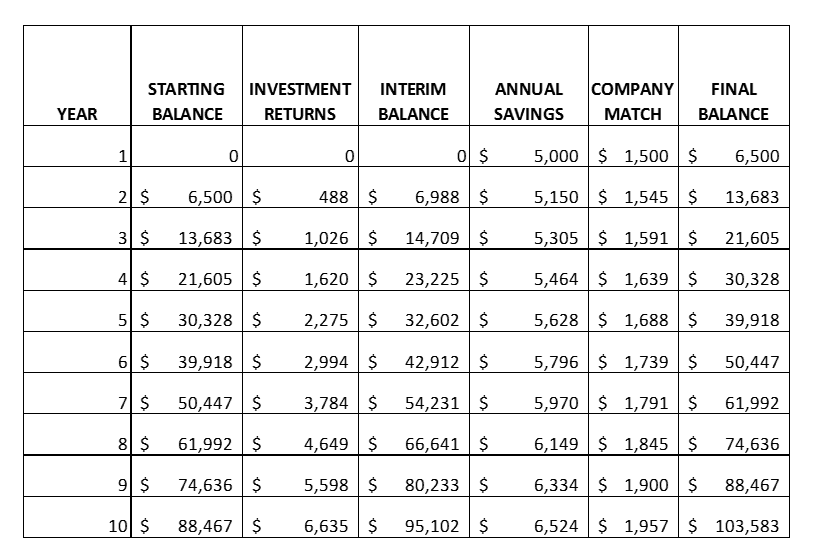

Let’s first look at how much money you’ll have left over to save for retirement each year assuming that you need to pay those student loans and are willing to save 10% of your salary:

Now, let’s take those savings numbers in the right hand column and see how you do with saving for retirement for the first 10 years of your working career:

In this scenario, after 10 years, you’ll have saved $14,562 which is at least a start at a nest egg, but only a fraction of what you could have saved.

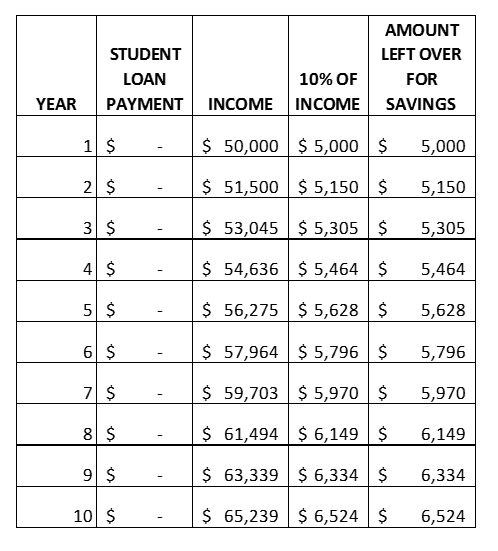

Here’s How It Looks Without the Debt

OK, same set up, but let’s now look at a scenario that you graduate debt-free from college. Here’s the amount of money you can save for retirement each year:

And here’s how that translates to the first decade of retirement savings:

Wow! That $37,000 in student loans resulted in a difference of about $89,000 ($103,583 – $14,562) in retirement savings at the end of 10 years once you factor in the company match that you miss out on and investment returns you can make along the way.

Here’s the Pay More Later Part

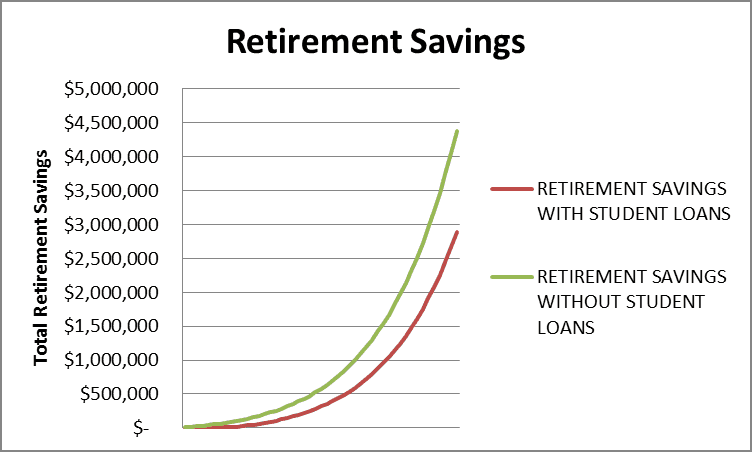

Of course, the difference keeps getting magnified to a larger and larger extent. If we assume that you work until age 70, here’s what happens over time to your retirement nest egg:

And while you might think, hey, no big deal, I’ll still have close to $3 million in the bank, we all know that “life happens” and you might want or need to save a little less each year for retirement so that you can:

- Purchase a first home

- Send your own kids to college at some point.

- Cover basic living expenses because you are unemployed for a period of time

- Open up a business that requires you to take a short-term hit in your income

- Retire early to pursue an Encore Career in a field you love.

Your Assignment:

Whether you are a high school senior trying to figure out where to go to school or a parent of a child wading through this decision, give serious consideration to options that allow the student to graduate with little or no debt. The Millennial Generation continues to feel the effects of being burdened with excessive student debt and, as you can see these effects carry forward throughout an entire working career.