3 Reasons Why Target Date Funds May be Off Target

Target Date Funds Are Popular, But Then Again, So Was Smoking

The use of Target Date Funds has become one of the most popular 401(k) options for retirement savers. According to this article, 71% of 401(k) plans offered a Target Date Fund option by the end of 2013 and 15% of all 401(k) assets are now parked in these products.

Admittedly, these funds are great if you’re looking for an autopilot version of retirement savings. You simply select the year you’d like to retire, choose the fund that most closely matches that timing and invest. The funds then act as a “set it and forget it” option by automatically moving your investments from being more risky when you’re in your 20’s, 30’s and 40’s to less risky as you approach retirement.

And while it’s appealing to many investors to utilize this approach, here are 3 reasons why Target Date Funds may be off target for you.

Reason #1 – Potentially Higher Fees

Target Date Funds are actually a “fund of funds.” This means that the Target Date Fund manager chooses a basket of ETF’s or mutual funds that comprise the Target Date Fund. Fees are then assessed both at the Target Date Fund level and at the underlying fund level as well.

And while a small difference in fees may not seem like a big deal, over a 30 or 40 year career they can have a huge impact on your overall retirement savings.

In fairness, not all Target Date Funds have high top level fees. For example the Vanguard Target Retirement 2050 Fund charges a top level fee of 0.16%. Look for options in this range if you choose to make this type of investment part of your retirement savings plan.

Reason #2 – Would You Consider Buying One-Size-Fits-All Shoes?

I’ve been doing some experimenting with Zappos.com for shoes recently and while I love the appeal of not having to drive to the store as well as free returns, the big obvious downside is it’s sometimes difficult to get shoes that fit well without trying them on first.

Retirement planning is a lot like shoe shopping. There is no one size fits all approach in terms of the types of investments you should make to fund the retirement you’re looking for. For some with ample savings, it may be perfectly fine to shed most of the equities out of your portfolio and focus more on the lower risk, safer returns that bonds have to offer. However, for others a different ratio of stocks and bonds may be more appropriate.

To get a feel for where you are in terms of your savings, consider calculating your Retirement Account Multiple to offer guidance on how aggressively you should be investing your retirement nest egg.

Reason #3 – “Safe” Investments Aren’t Necessarily Safe

This is really a subset of Reason #2 above, which is some Target Date Funds may be too conservative to adequately fund your retirement. In a previous post, I showed how moving out of stocks and into ultra conservative investments at age 50 could cut your retirement income nearly in half based on historical returns. And while we know that the historical returns of stocks are no guarantee of future results, it’s the best information we have available to guide our decisions.

In the article, “A Dynamic Yield Curve-Based Approach to Retiree Portfolio Allocation,” authors Jason Fink and Kristin Fink make a compelling argument based on the analysis of historical data from 1926-2015 that retirees should maintain an allocation of between 50%-75% in stocks throughout their retirement to maximize the odds that they will not outlive their money.

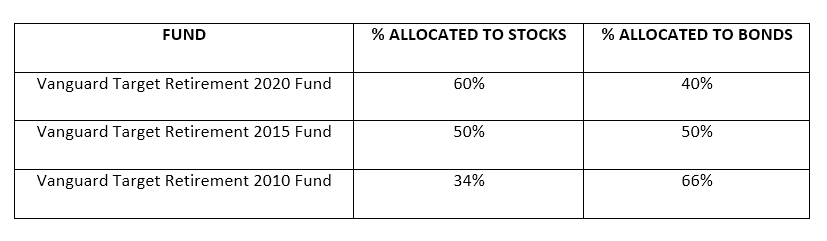

In the context of the above referenced article by Fink & Fink, let’s look at the allocations of three Target Date Funds:

The best way to know how much risk you need to take with your retirement savings is to work with a qualified financial advisor to construct a Retirement Plan based on your current level of savings, your plans for full- or semi-retirement and most importantly, the goals and passions you’d like to pursue to enjoy the fruits of your many years of labor.So, if you turned 65 in 2010 and retired with the majority of your 401(k) in the Vanguard 2010 fund, you may not be properly allocated across stocks and bonds to achieve the standard of living you’re looking for in retirement.

Your Assignment:

Whether you’re approaching retirement or are already retired, take a closer look at Target Date Funds if you have a significant fraction of your retirement savings invested there. Watch out for high fees and be aware that the one-size-fits-all approach that these funds offer may or may not be appropriate for you. Taking the time to do so now can potentially pay huge dividends and help you create the kind of retirement you’ve always wanted!